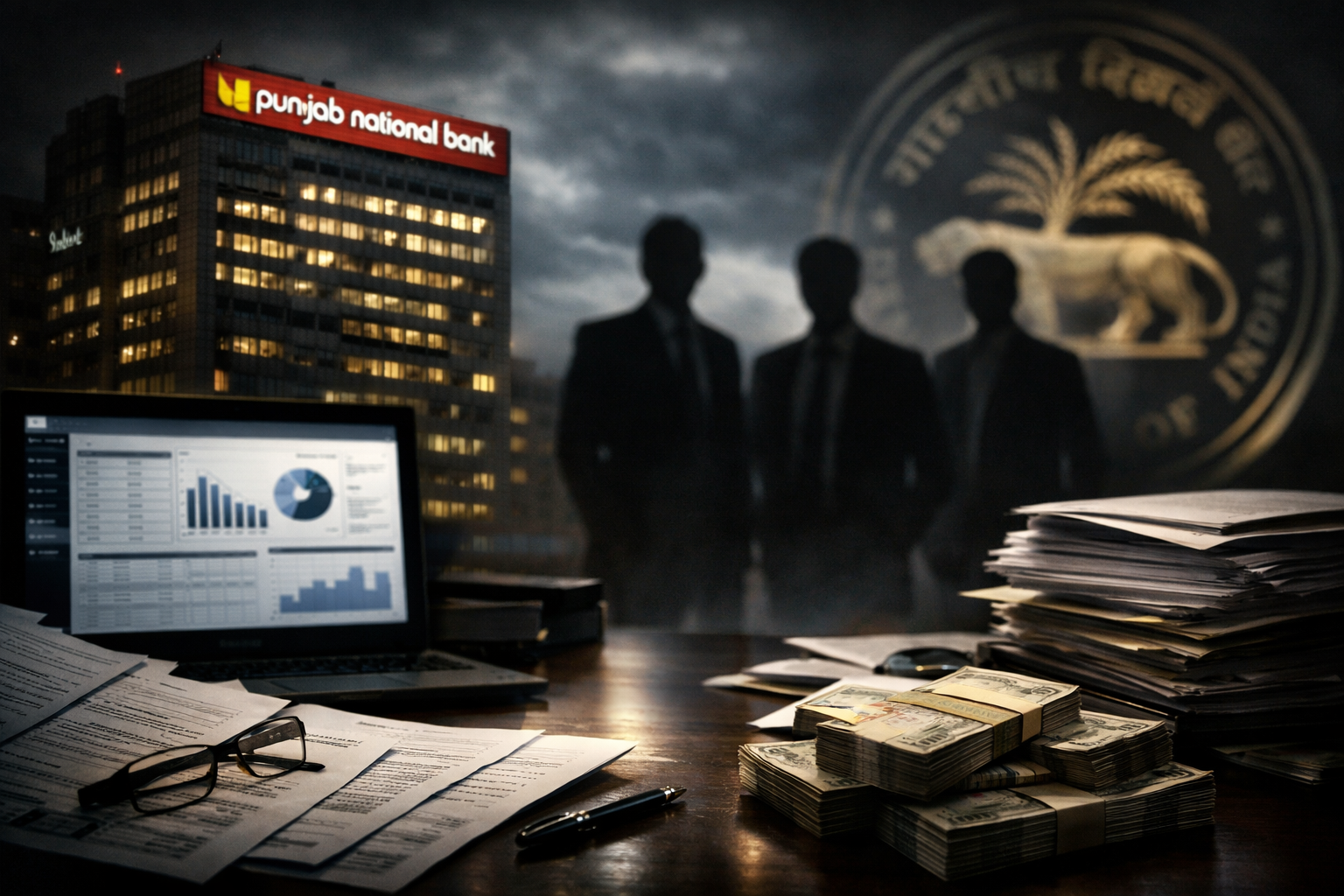

Punjab National Bank (PNB) has officially reported a loan fraud worth approximately ₹2,434 crore to the Reserve Bank of India (RBI), linked to the former promoters of SREI group companies. This development has created serious buzz in India’s financial and banking sector because it once again highlights how big corporate loan frauds continue to affect the banking ecosystem.

Punjab National Bank (PNB) has officially reported a loan fraud worth approximately ₹2,434 crore to the Reserve Bank of India (RBI), linked to the former promoters of SREI group companies. This development has created serious buzz in India’s financial and banking sector because it once again highlights how big corporate loan frauds continue to affect the banking ecosystem.

In this detailed blog, we will break down:

-

What exactly happened in this SREI loan fraud case

-

How the fraud reportedly took place

-

What the forensic audit and internal review revealed

-

Its similarities with previous high-profile fraud cases like Nirav Modi

-

And what this means for the banking sector and Indian economy

The aim of this article is to keep the information easy to understand, SEO-friendly, clear, and structured, so every reader can understand the reality behind this massive financial scandal.

What Is the SREI Loan Fraud Case?

Punjab National Bank reported that loans given to SREI Infrastructure Finance Ltd and SREI Equipment Finance Ltd turned doubtful, after which investigations and reviews began. According to PNB’s findings, the total detected fraud amount is ₹2,434 crore.

These loans were originally given to support infrastructure financing and development. However, investigations suggested otherwise — and what came out was shocking for the banking regulator, investors, and the public.

Why Is This News So Important?

Because this is not just about one company.

This is about:

-

Trust in India’s banking system

-

Accountability of big corporate borrowers

-

Safety of public money deposited in banks

Whenever such big frauds are exposed, it automatically reminds the public of cases like:

-

Nirav Modi – ₹14,000 crore PNB scam

-

Vijay Mallya loan default

-

ABG Shipyard fraud case

The SREI case once again raises questions on:

-

Due diligence by banks

-

Loan monitoring systems

-

Corporate governance ethics

What Did PNB Tell the RBI?

PNB officially informed the Reserve Bank of India that the SREI accounts have been classified as fraud after a detailed review. Reporting to RBI is mandatory under banking regulations once fraud is established.

This report means:

-

RBI is now officially aware

-

Regulatory scrutiny will increase

-

Legal and financial consequences will follow

How Did the Fraud Allegedly Happen?

According to the findings revealed, the fraud mainly took place through:

✔ Misrepresentation of Asset Values

The borrowers allegedly showcased inflated asset values.

This created a false picture of:

-

Strong financial stability

-

Good business liquidity

-

Higher repayment ability

Banks rely heavily on documented financial strength to approve such massive loans. When those documents themselves are misleading, fraud becomes easier.

✔ False Representation of Repayment Capacity

Documents reportedly claimed that the company had strong repayment capability.

In reality, the borrowers allegedly did not have the financial strength to repay dues.

This created a gap between:

-

What was shown

-

What actually existed

✔ Diversion of Funds

The most serious allegation is fund diversion.

Forensic and internal reviews conducted by Punjab National Bank revealed that:

-

The loan money was not used for business purposes

-

Funds were reportedly moved elsewhere

-

Money may have been channelled into unrelated activities

This is a clear violation of lending norms.

Forensic Audit and Internal Review Findings

The case did not come to light suddenly.

It took detailed investigation.

PNB conducted:

-

Internal financial reviews

-

Forensic audits

-

Loan usage tracking

These investigations found multiple irregularities.

Based on this strong evidence, the bank decided to officially declare the account as fraudulent.

This step is important because:

-

It allows legal action

-

Enables asset recovery processes

-

Strengthens financial discipline

Comparison With Previous High-Profile Fraud Cases

Many experts are comparing this incident with the Nirav Modi PNB Scam, because:

✔ Both involve huge financial amounts

Thousands of crores lost, impacting banking sector stability.

✔ Both highlight system loopholes

Weak monitoring, delayed detection, and trust misuse.

✔ Both create fear among depositors and investors

People worry about safety of funds when such cases repeat.

However, while every case has different technical details, the common message remains the same:

Strong banking governance is essential.

What Happens Next?

Now that the fraud has been officially declared, multiple steps may follow:

-

RBI supervision and monitoring

-

Legal proceedings against those involved

-

Possible enforcement actions

-

Asset seizure and recovery attempts

-

Accountability investigations

Authorities will try to determine:

-

Who was responsible

-

Where the money went

-

How to recover it

Impact on the Banking Sector

Such massive fraud cases don’t just hurt one bank.

They affect the entire financial system.

Impact 1: Loss of Public Money

Banks operate on depositor’s money.

When loans turn fraudulent, the burden indirectly falls on:

-

Government

-

Banking system

-

Common citizens

Impact 2: Increased Strictness in Lending

Banks will now:

-

Tighten lending rules

-

Increase background checks

-

Strengthen verification processes

This may make it slightly harder for genuine businesses to borrow too, but it increases overall financial security.

Impact 3: Damage to Market Confidence

Every major fraud shakes:

-

Investor confidence

-

International financial reputation

-

Market stability

But exposing frauds also shows India’s banking sector is becoming stricter and more transparent.

Why This Case Matters for India

India is pushing big-time toward infrastructure development and corporate growth.

To achieve that, banks must be strong and trustworthy.

Cases like this highlight:

-

The importance of transparency

-

The need for ethical corporate behavior

-

Stronger financial regulations

Final Words

The ₹2,434 crore PNB – SREI fraud case is another big reminder that financial discipline and honesty in corporate borrowing are essential. Punjab National Bank’s decision to report this fraud to the RBI is a crucial step toward accountability.

From misrepresentation of assets to diversion of funds, the case reflects deep financial irregularities. As legal and regulatory processes begin, the outcome will not only impact the involved parties but will also shape future banking policies.

The hope is clear:

-

Stronger systems

-

Safer banks

-

More responsible borrowing

-

And protection of public money

This story is still developing, and further actions and investigations will decide how it unfolds.